Potential Changes to the IRS Offshore Voluntary Disclosure Program (OVDP)

U.S. taxpayers who have foreign bank and/or financial accounts should be watching the clock. The window to voluntarily report foreign accounts in order to mitigate IRS penalties may be at the end of 2017. Like all IRS amnesty programs, the Offshore Voluntary Disclosure Program (OVDP) was not meant to be left open indefinitely. While the voluntary disclosure programs have been proven to be quite effective and lucrative for the IRS, there are four significant reasons the program will likely come to an end in 2017. The Wolf Group takes an in-depth look at the reasons for the program’s potential closure and what taxpayers with foreign bank and financial accounts should be doing now to mitigate the penalties that they may otherwise be subject to after the end of 2017.

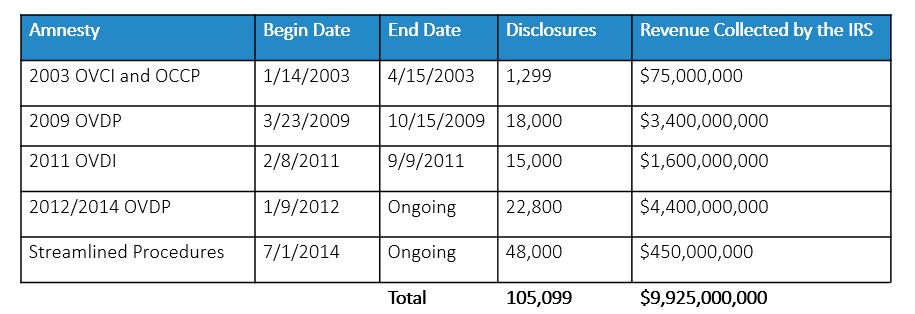

Amnesty programs generally end – listed below are some examples[1]:

What is OVDP?

What is OVDP?

OVDP is an amnesty program that falls under IRS voluntary disclosure practice (see IRM 9.5.11.9)[2] . The program provides taxpayers with a path to resolve previous omissions, errors, and unreported forms while mitigating the potential penalties of continued non-compliance. Under normal IRS procedures, once detected, a taxpayer would be placed under audit procedures, assessed penalties for all failure to file informational reports such as FBARs, and taxes, interest, and all associated penalties for failing to report associated income such as interest, dividends, and capital gains from the foreign financial account(s). If the error has a basis of criminality, the taxpayer may be referred to Criminal Investigations for criminal penalties and/or prosecution. This can be quite expensive for both the IRS and the taxpayer. Additionally, the IRS has identified that the number of individuals that could have issues that fall within this realm is substantial (i.e., well beyond the 105,099 disclosures submitted to date). In lieu of this, if the taxpayer voluntary comes forward and discloses this information under OVDP, then the associated penalties to the taxpayer will be far less than if they were detected and undergone a full audit.

Why It Is Likely That OVDP Is Ending

Having serviced some of the most complex OVDP cases and navigating the tangled rules of OVDP compliance since the program’s inception, The Wolf Group takes a look at the four significant reasons why the OVDP program will likely come to an end in 2017.

1. The IRS does not have sustainable staffing on its present and prospective budgets. President Trump recently called for a $239 million cut to the IRS budget in 2018. The proposed spending cut is similar to a reduction proposed in the House last year and represents about 2% of the budget. This alone is not enough but taken in conjunction with recent historical budget cuts and/or lack of increased budgets the IRS staffing has decreased 30%[3] over the last couple of years. The average OVDP takes roughly 2 years to complete from submission to receipt of the closing form 906. There are multiple administrative, examination, technicians, and managers involved in this process, especially if there is an opt-out. The amount of time, energy, and resources that the IRS must allocate to this area cannot be sustained. This is akin to the status of normal IRS audit or examination. In that area, the IRS has been very created and resorted to automated matching and computer generated notices as a substitute to the lack of workforce.

2. The Foreign Account Tax Compliance Act (FATCA)[4] and Intergovernmental Agreements (IGAs) have produced a treasure trove of information that has been exchanged between foreign countries and the US. Most of the agreements have been in place since 2014 with most information being shared between 2015 and the current year. As mentioned above, like IRS normal audit or examination, the IRS could use this information to conduct a match against tax returns and FBARs that have been filed to see which taxpayers may have delinquent (or inaccurate) FBARs and 8938s. They could then use this information to generate computer notices with informational penalties.

3. The third reason is the ICIJ Panama Papers case. The panama papers leaked offshore holdings from 1977 to 2015. The papers revealed 11.5 million records including the holdings of 140 politicians, 214,088 offshore entities, and 33 persons/companies blacklisted by the US government[5]. This information is public and can be readily used by the IRS as an investigative and matching tool. The offshore entity disclosure is particularly intriguing. With a targeted John Doe Summons, these entities could further produce undetected individuals or companies.

4. With over 100,000 disclosures in the previous and current OVDP programs it must be noted that the IRS uses the information it receives to conduct internal data mining. The data mining can be used to identify taxpayers that have not voluntarily disclosed information, businesses or entities in tax havens that need further scrutiny via John Does Summons, and/or the paper trail showing the flow of unreported funds from tax haven country to tax haven country.

What Should Taxpayers with Undisclosed Accounts Do Next?

Before considering next steps, taxpayers should decide on what to do now. Taxpayers with willful noncompliance should enter the full Offshore Voluntary Disclosure Program as soon as possible. The potential criminal exposure is significant otherwise.

Taxpayers that are non-willful and currently setting up for a Streamlined Filing or considering a Streamlined Filing, should get this process started as early as possible. Unlike OVDP, Streamlined Filing does not have a pre-clearance or acceptance process before submission. The IRS will not know about the disclosure until it is submitted to them. The submission requires three years of delinquent or amended tax returns plus six years of FBARs. The time needed to correctly put together one of these submissions can be extensive. Therefore, planning accordingly and allowing enough time to gather all the information needed, provide representatives with this information via their internal organizers and format, and follow their internal procedures for review and submission. The goal simple. The submission must be clean, comply with all of the Streamlined Procedure rules, and easy to follow for IRS processing.

Should these programs close before a taxpayer can get an accepted pre-clearance under OVDP or submission for Streamlined Filing, then one must revert to the standard Voluntary Disclosure Practice under IRM 9.5.11.9. Most practitioners are familiar with OVDP but very few are familiar with the VDP practice that was enacted prior to 2009. These practitioners will be few and far in-between so verifying the practitioner’s experience in this area is essential. VDP may end up looking like the current versions of OVDP and Streamlined Procedure but there will be much more work at the beginning with the disclosure of facts and the agreed upon terms for submission.

For those that receive automated notices with FBAR, 8938, and/or other international informational related penalties, they should immediately seek a firm that has experience representing taxpayers with the IRS international audit team.

Contact:

The Wolf Group has assisted hundreds of clients in making voluntary disclosures of unreported foreign accounts in order to avoid the draconian penalties that may be assessed by the IRS. Please contact our New Client Lead, Fan Chen, at 703-652-1737 or at fanchen@thewolfgroup.com to learn how we can help with U.S. tax compliance complexities

[1] https://www.irs.gov

[2] https://www.irs.gov/irm/part9/irm_09-005-011-cont01.html#d0e1302

[3] http://www.latimes.com/politics/washington/la-na-essential-washington-updates-trump-budget-to-slash-irs-funding-1489665882-htmlstory.html

[4] https://www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA.aspx

[5] https://en.wikipedia.org/wiki/Panama_Papers